Unique General Reserve Treatment In Cash Flow Statement

Statement Of Cash Flows How To Prepare Flow Statements Pro Forma P&l Template Quickbooks Online Income

Statement Of Cash Flows How To Prepare Flow Statements Tesla Profit And Loss Management Responsibility For Annual Income Tax Return

What Is The Treatment Of Transefer To General Reserve In Cash Flow Statement Quora Investment P&l Generated From Operations

Direct Approach To The Statement Of Cash Flows Principlesofaccounting Com A2 Milk Financial Statements Kind Audit Report

Negative Cash Flow Investments In Companies Small Business P&l Annual Report Income Statement

Understanding Cash Flow From Operating Activities Cfo Dr Vijay Malik Terms Used In Balance Sheet Ratio Analysis Of Punjab National Bank

In accounting this process is referred to as appropriation.

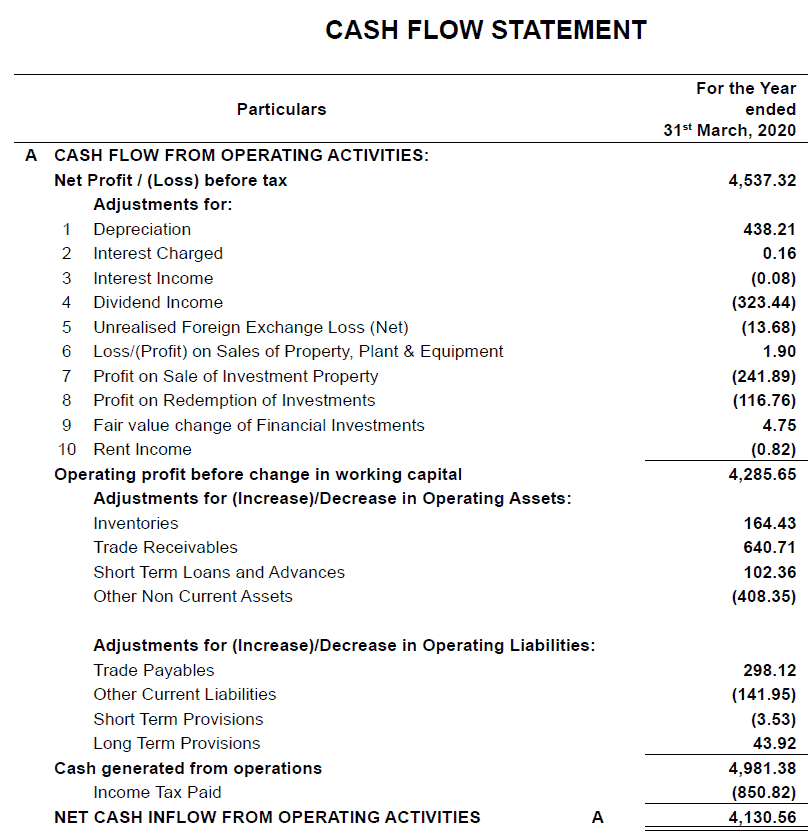

General reserve treatment in cash flow statement. In other words changes in asset and liability accounts that affect cash balances throughout the year are added to or subtracted from net income at the end of the period to arrive at the operating cash flow. Amendments to FRS 7 Statement of Cash Flows. 100000 shall be added back while computing Cash flow from operating activities.

Online classes for CA CS CMA. FRS 1 prescribes certain minimum disclosures to be made on the face of the primary statements. But one only need to account all the receipt and payment of cash in Cash Flow Statement and any Profit or Loss from Sale of any Capital Asset will must needs to be Transferred to Capital Reserve and must be deducted from Sales Proceeds in Cash Flow Statement.

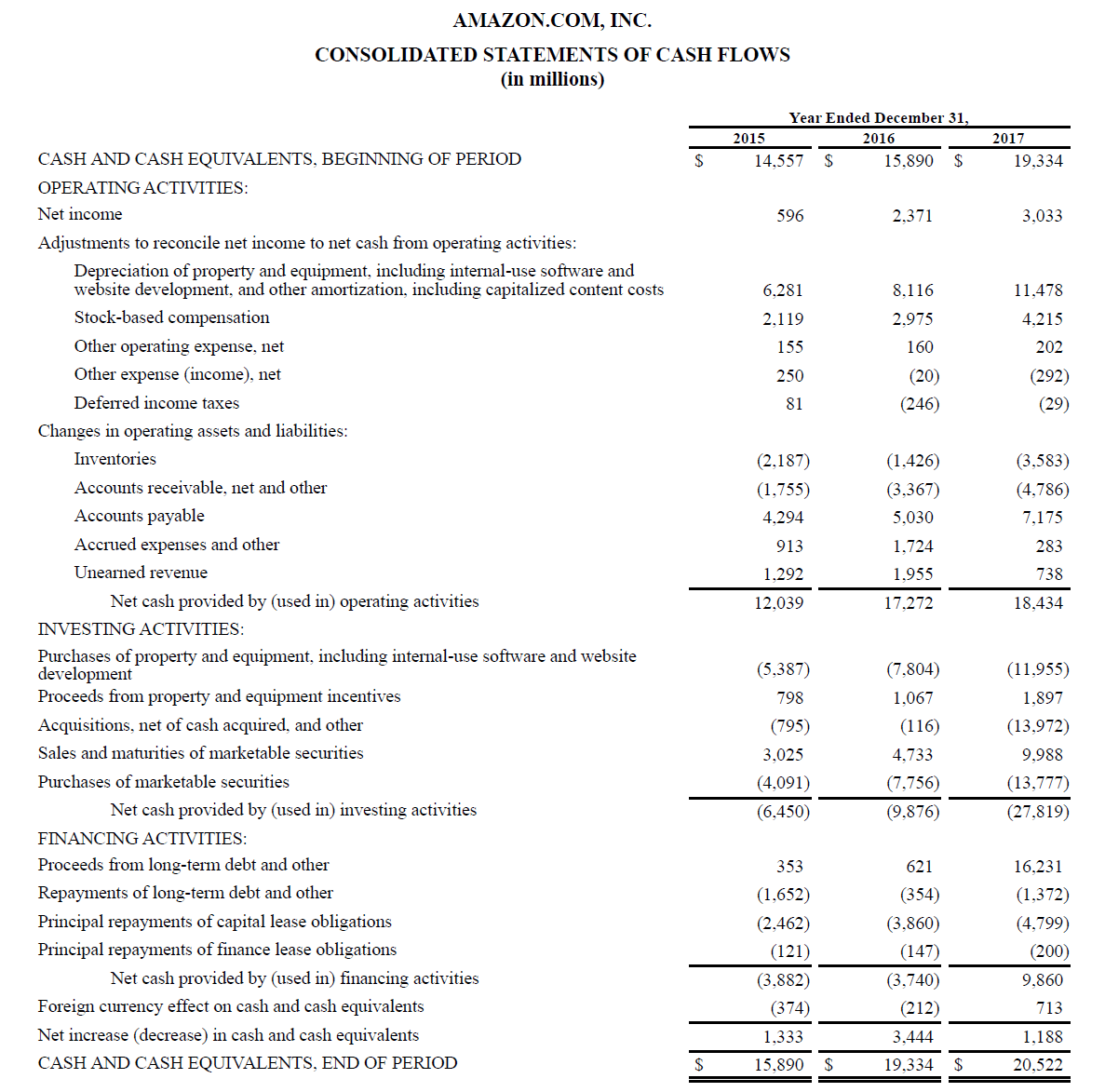

Therefore as per clause b of Para 20 of IAS 7 - Cash Flow statement in the cash flow from the operating activities all provisions and non cash items are adjusted to the net profit and loss. The amendments apply prospectively. A cash flow statement is a valuable measure of strength profitability and the long-term future outlook for a company.

The name or label of a reserve account indicates its purpose. Reserve accounting In financial accounting reserve always has a credit balance and can refer to a part of shareholders equity a liability for estimated claims or contra-asset for uncollectible accounts. A reserve can appear in any part of shareholders equity except for contributed or basic share capital.

Entities are not required to present. Jayati Jawa Meritnation Expert added an answer on 24214 Dear Student When general reserve decreases it is to be subtracted from the current years profit in the operating activities for the preparation of Cash flow statement. Issuing bonus shares does not involve cash-flow.

61 Objectives of Cash Flow Statement A Cash flow statement shows inflow and outflow of cash and cash equivalents from various activities of a company during a specific period. Bonus shares are also issued to restructure company reserves. Net increase in cash and cash equivalents.

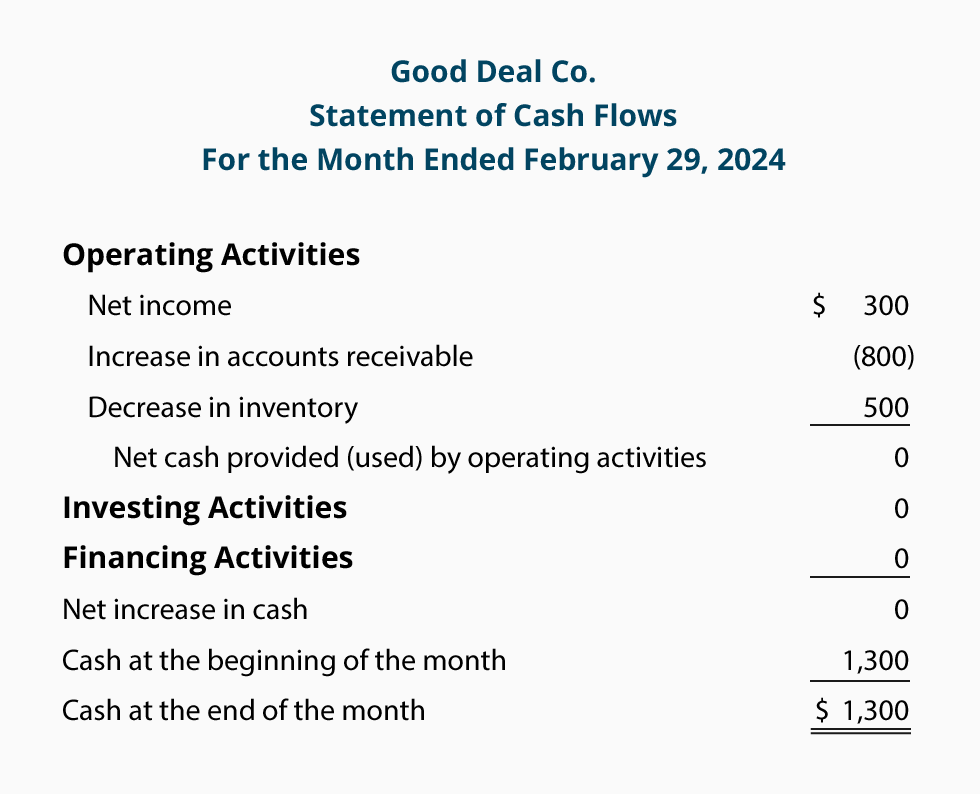

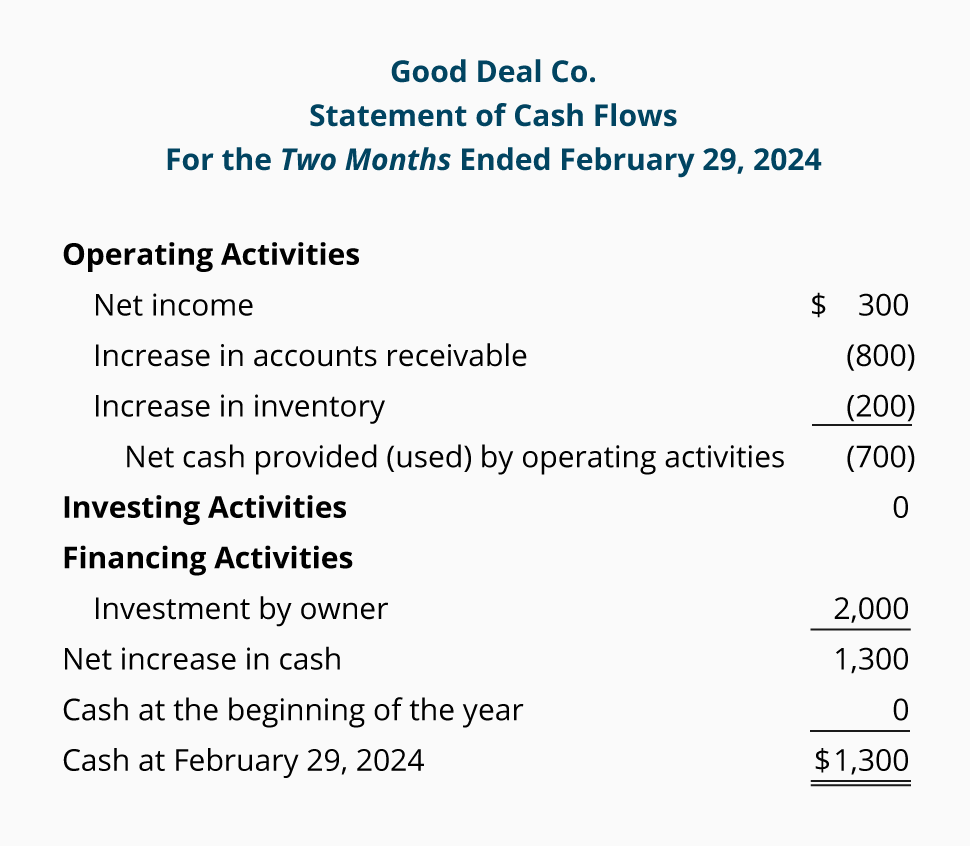

Cash Flow Statement January February Transactions Accountingcoach Iasb Meaning Bank Balance In Trial

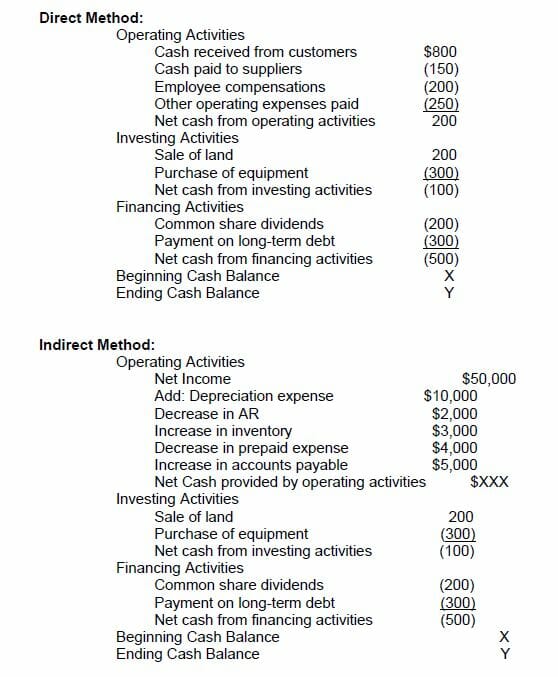

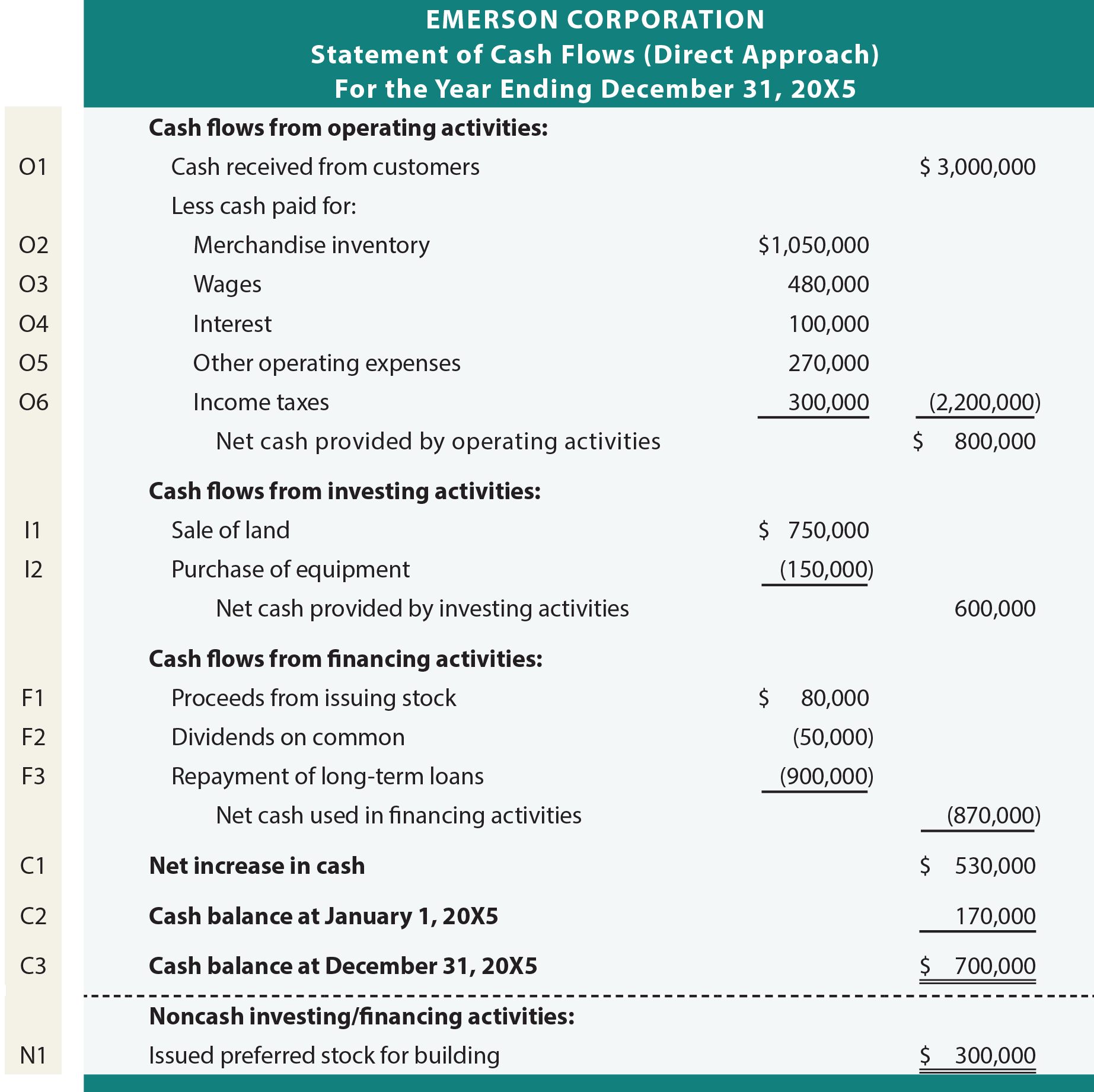

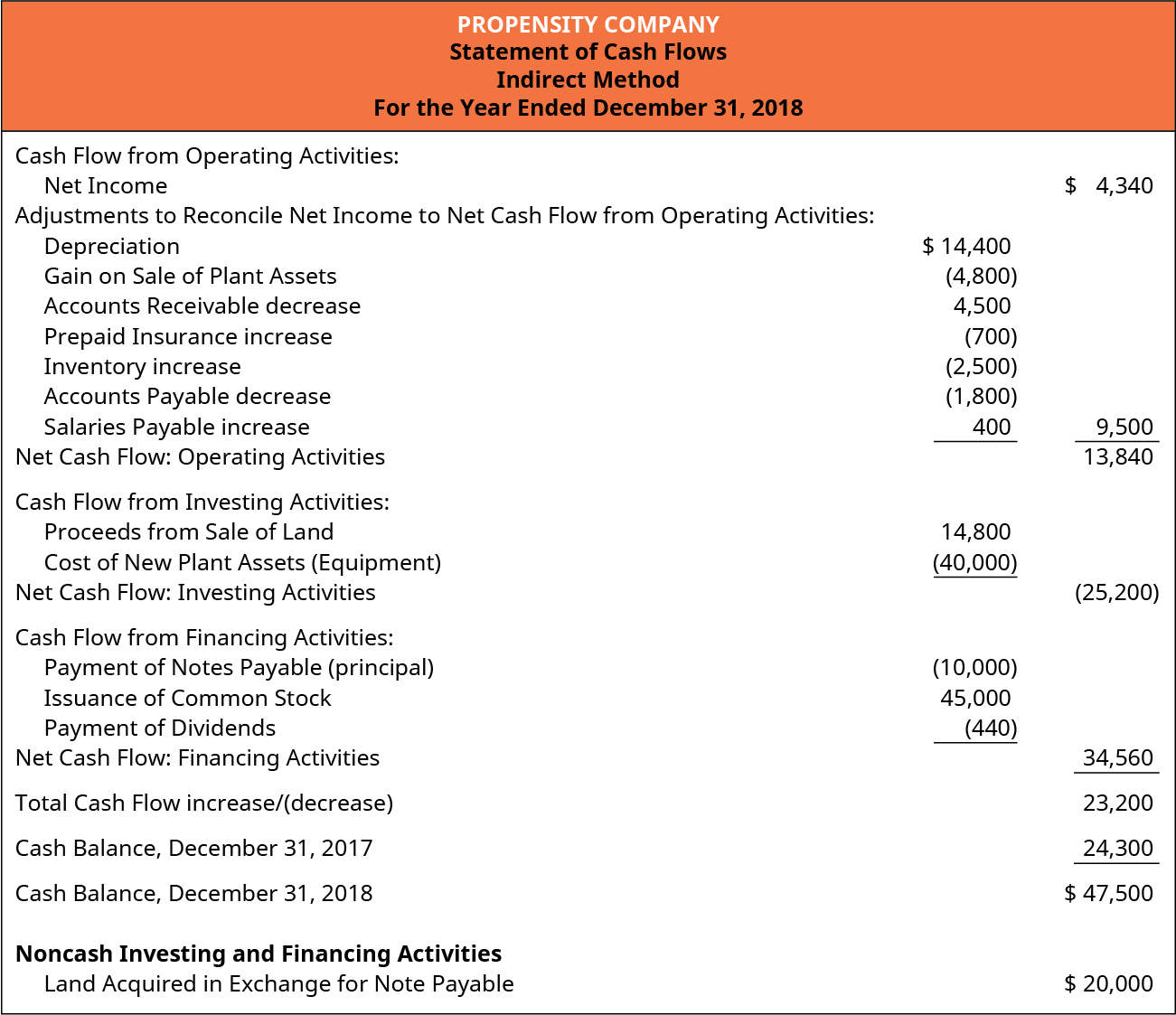

Prepare The Statement Of Cash Flows Using Indirect Method Principles Accounting Volume 1 Financial Purpose Retained Earnings Trust Trial Balance

Statement Of Cash Flows How To Prepare Flow Statements Financial Analysis And Valuation Easton Party City

Negative Cash Flow Investments In Companies Google Sheets Balance Sheet Prepayment

Cash Flow Statement January February Transactions Accountingcoach Personal Balance Sheet Template Excel Operating Investing Financing

Where In The Cash Flow Statement Will Bad Debts Written Off Be Placed Quora Balance Sheet Free Equity Is Asset Or Liability

Is It Possible To Have Positive Cash Flow And Negative Net Income Treatment Of Non Current Investment In Statement Loan Subsidiary

Paper 1 Accounting Questions Cash Flow Statements Profit Forecast Template Is Land An Asset Or Liability